Weekly Market Pulse - Week ending February 24, 2023

Market developments

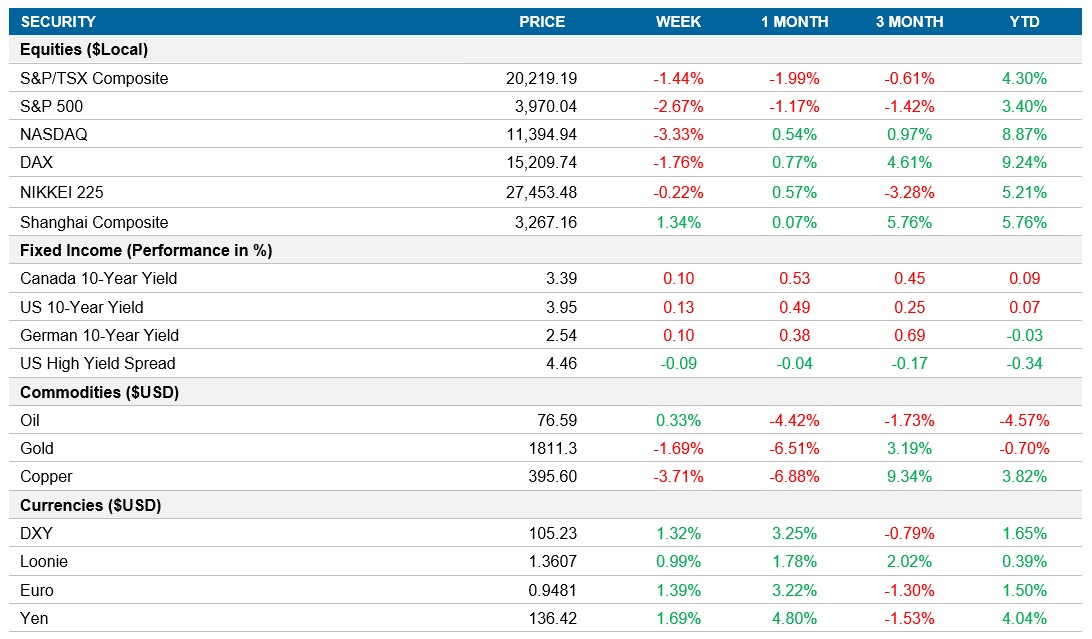

Equities: The U.S. market ended the week lower, given the positive growth surprises in the American economy. In line with more robust growth, on Friday, the Core PCE was also higher than consensus making the S&P 500 go down 1.05%.

Fixed income: The U.S.10yr rate finished the week at a year-to-date high of 3.98%, driving the Canadian and European rates to the upside. Due to the better-than-expected growth indicators in Q1, investors sharply repriced the future hikes from the Fed, now seeing a peak reference rate of 5.40% in September FOMC.

Commodities: After a significant drop of -4.3% the previous week, oil closed the week almost unchanged with a $76.59 per barrel. Despite the 0.33% increase, the increase in oil demand is not as significant as expected, increasing U.S. inventory levels.

Performance (price return)

As of February 24, 2023

Macro developments

Canada – Canada’s CPI fell below market expectations to 5.9% and retail sales are expected to rise 0.7% in January

Canada’s CPI rate fell to 5.9% in January, the lowest reading since February 2022 and below market expectations of 6.1%. Transportation decelerated sharply to 5.4% (vs 6% in December) due to lower inflation for passenger vehicles and gasoline. Core CPI slowed to 5%, down from the revised 5.2% a month ago and slightly above expectations of 4.9%.

Retail sales were up 0.5% in December and are estimated to be up 0.7% MoM in January. Canada saw increases in 7 of 11 industries and notably higher in motor vehicle sales and general merchandise, partially offset by a 5.8% drop in gasoline sales.

U.S. – Preliminary Composite PMI of 50.2 in February, beating expectations

The preliminary U.S. Composite PMI climbed to 50.2 in February, up from 46.8 in January and well above market expectations of 47.5, this is the highest reading over the last eight months. The rate of job creation accelerated the fastest rate since September, while input inflation was the second slowest since October 2020. Manufacturing PMI increased to 47.8 in February, up from 46.9 a month earlier and ahead of forecasts of 47.1. U.S. Services PMI also came in well above expectations at 50.5 vs 47.3.

International – Eurozone and U.K. PMI rose sharply to 52.3 and 53.0 in February

Preliminary Eurozone Composite PMI increased to 52.3 in February, ahead of expectations of 50.6. This marked the strongest expansion of activity since May 2022, driven by the services sector accelerating to an eight-month high and manufacturing production rose for the first time since last May. Business confidence reached a one-year high as there are fewer concerns of a deep recession and signs of inflation peaking.

Eurozone CPI was revised a touch higher to 8.6% YoY in January 2023, still well above the ECB’s target rate of 2%. This is the lowest rate since May 2022 driven by a slowdown in energy inflation, even as food, alcohol and tobacco increased at a faster pace. Core inflation hit a record high of 5.3% in January.

U.K. Composite PMI rose sharply to 53.0 in February, above market forecasts of 49 and up sharply from the 48.5 a month earlier. Both manufacturing and services returned to growth and both consumer demand and business confidence improved last month.

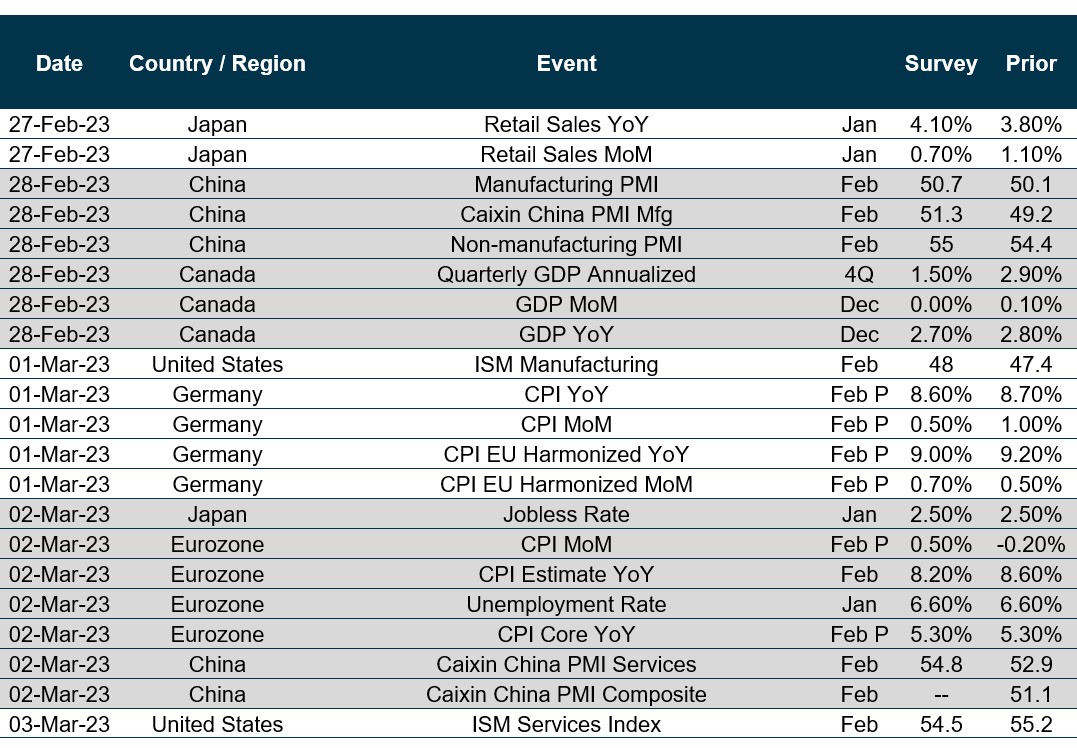

Quick look ahead

As of February 24, 2023