Weekly Market Pulse - Week ending May 17, 2024

Market developments

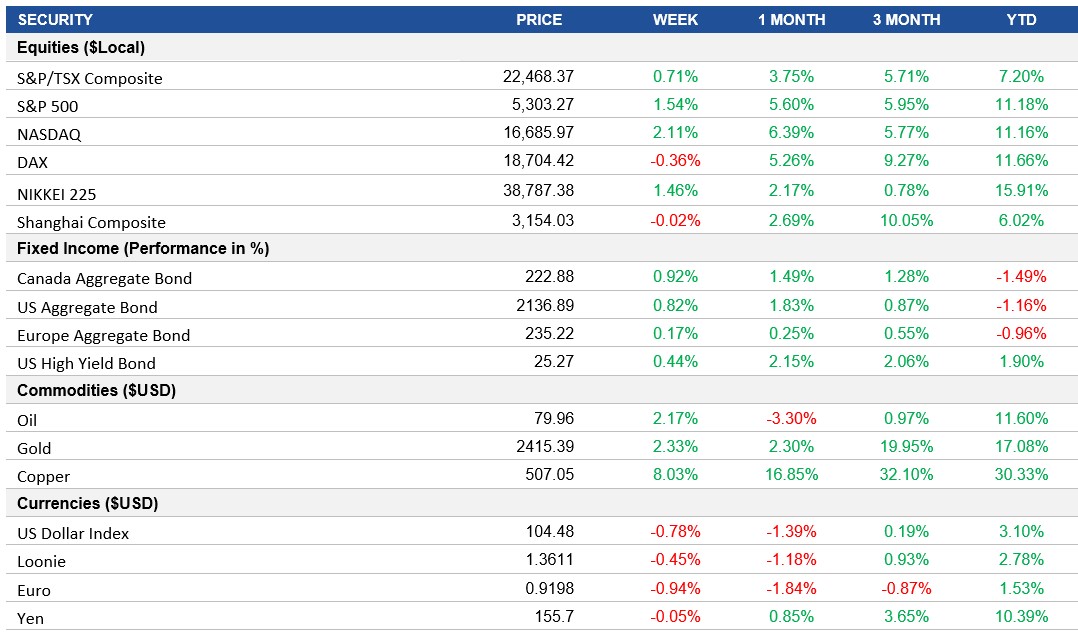

Equities: The stock market has been rallying recently, with the S&P 500 on track for its fourth straight weekly gain. This has been fueled by hopes of Federal Reserve rate cuts following some positive inflation reports, as well as strong corporate earnings, particularly in the AI sector with Nvidia's upcoming results in focus. The meme stock frenzy cooled, with GameStop plunging on plans to sell more shares and the rally lost some steam over the past two days as the market consolidated its gains. The S&P 500 hovered near 5,300, while the Dow Jones Industrial Average fluctuated around 39,900 after briefly crossing 40,000 for the first time.

Fixed Income: After the recent inflation reports, housing data, and retail sales figures, the market is trying to assess whether the economy is moving in a direction that would allow the Federal Reserve to cut interest rates. The mixed economic data has created uncertainty about the Fed's next moves, with some analysts tempering expectations for significant rate cuts in the near term. However, as macroeconomic conditions soften, strategists, like at Bank of America, expect a resurgence in long-duration bonds later in 2024.

Commodities: Oil rose back around $80 per barrel on Friday for the first time this month, ahead of the June 1 OPEC+ meeting. The rise in crude prices this week reflects anticipation around factors that could boost demand (U.S. driving season, rate cuts) and tighten supply.

Performance (price return)

Source: Bloomberg, as of May 17, 2024

Macro developments

Canada – No Notable Releases

No notable releases this week.

U.S. – U.S. Inflation Eases Slightly in April 2024, U.S. Retail Sales Remain Unchanged in April 2024

The annual inflation rate in the U.S. eased to 3.4% in April 2024 from 3.5% in March, aligning with market expectations. Inflation steadied for food and slowed for shelter, while prices for new and used vehicles continued to decline. Energy costs rose slightly, with increases in gasoline but declines in utility gas and fuel oil. Transportation and apparel costs rose faster. The CPI increased by 0.3% monthly, below previous months and forecasts, while core inflation slowed to 3.6% annually, the lowest since April 2021.

Retail sales in the U.S. were flat in April 2024, following a revised 0.6% gain in March, contrary to forecasts of a 0.4% rise, indicating a slight easing in consumer spending. Declines were seen in 7 out of 13 categories, including non-store retailers and motor vehicles. Sales increased at gasoline stations, clothing stores, and electronics stores. Core retail sales, which exclude certain categories and are used to calculate GDP, edged higher by 0.2%.

International – U.K.'s Unemployment Rate Rises to 4.3%, Eurozone Economy Rebounds in Q1 2024, Japan's GDP Shrinks by 0.5% in Q1 2024, China's Inflation Rate Rises to 0.3% in April, China's Retail Sales Growth Slows to 2.3% in April

The U.K.'s unemployment rate increased to 4.3% from January to March 2024, up from 4.2% in the previous three months, matching market expectations. The number of unemployed rose by 46,000 to 1.49 million, driven by short-term unemployment, while long-term unemployment also increased. The number of employed individuals rose by 17,000 to 33 million.

The Eurozone economy grew by 0.3% in Q1 2024, recovering from contractions in the previous two quarters and marking the strongest GDP growth since Q3 2022. German GDP rebounded, growth in France and Italy accelerated, while Spain's economy maintained robust growth. After stagnation in 2023, the Eurozone is on a recovery path, with inflation nearing the 2% target. The European Commission forecasts 0.8% growth for 2024, driven by consumer spending and trade, though investment growth is softening.

Japan's producer prices increased by 0.9% year-on-year in April 2024, consistent with market expectations, marking the 39th consecutive month of growth. Prices rose for various components, including transport equipment and beverages, while costs fell for chemicals and iron & steel. Monthly, producer prices rose by 0.3%, the highest increase in four months.

China's annual inflation rate increased to 0.3% in April 2024, up from 0.1% in March, amid recovering domestic demand. Non-food inflation accelerated, with higher prices for clothing, housing, health, and education. Transport costs rose after previous declines. Food prices continued to fall for the 10th month. Core consumer prices, excluding food and energy, increased by 0.7% year-on-year. Monthly, the CPI rose by 0.1%, reversing from a significant fall in March.

China's retail sales grew by 2.3% year-on-year in April 2024, below market forecasts and the previous month's growth, indicating challenges in boosting consumption despite government stimulus. Growth slowed for grain, home appliances, and oil products, while turnover declined for clothing and cars. Sales quickened for personal care, furniture, and communications equipment. Monthly retail trade was nearly flat, and retail turnover for the first four months grew by 4.1%.

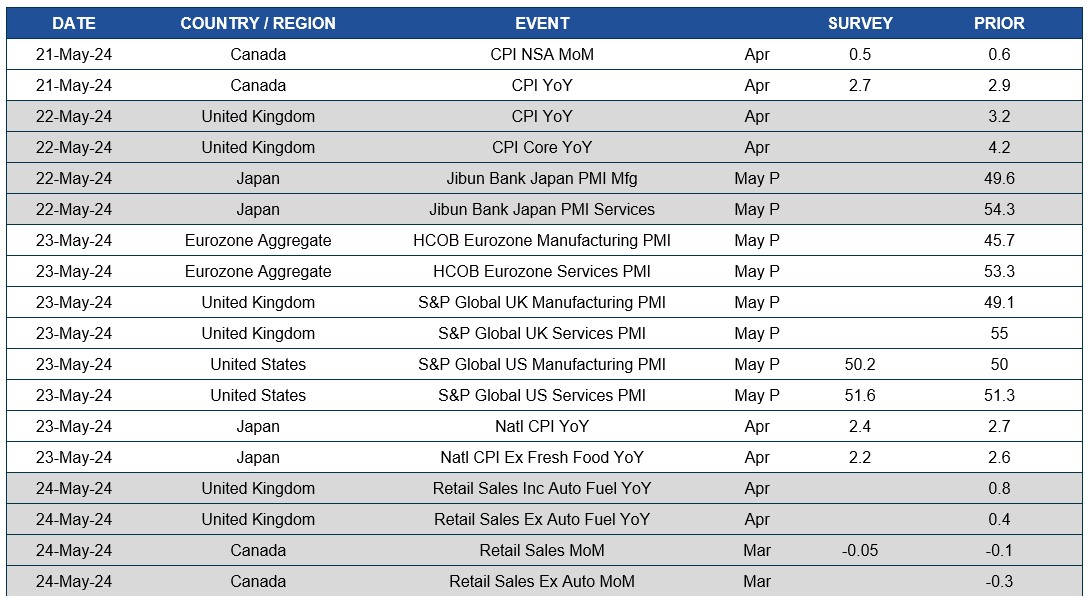

Quick look ahead

As of May 17, 2024