Weekly Market Pulse - Week ending September 20, 2024

Market developments

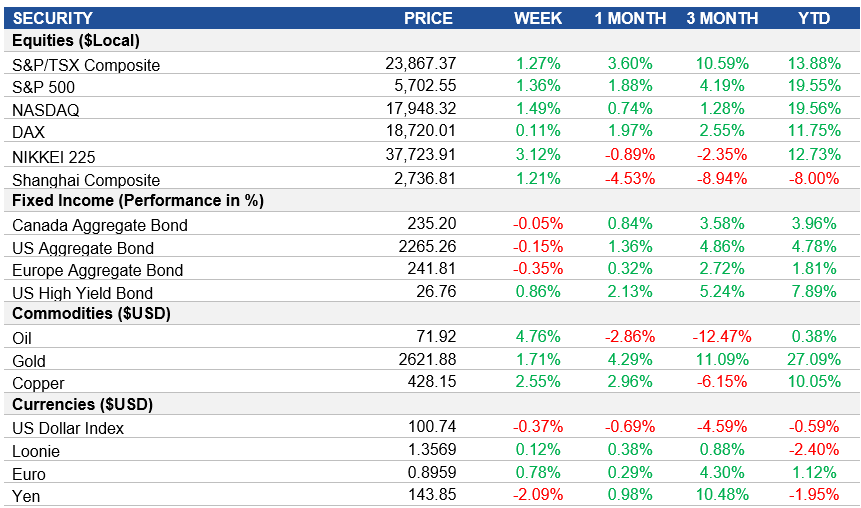

Equities: The S&P 500's reached its 39th record high in 2024 and climbed over 1% this week following the Federal Reserve's recent half-point rate cut. Despite the recent optimism from the Fed's actions, analysts warn of underlying economic risks as some strategists believe the current equity market optimism could signal a risk of a bubble, making bonds and gold appealing as hedges against potential recession or inflation.

Fixed Income: Even with the Federal Reserve's recent half-point rate cut, Treasury yields increased this week, driving bond indices lower. This was driven by a shift in the dot plot, which now suggests that the Fed is ready to implement an additional 50bps of cuts for the remainder of this year (25bps less than what the market has priced in).

Commodities: The Fed's recent cut was seen as a strong start to a new easing cycle, which is generally bullish for gold as lower rates reduce the opportunity cost of holding non-yielding assets like bullion. Even as gold hits new all-time highs, analysts anticipate a potential short-term pullback due to extreme positioning among investors. However, they expect falling rates to support gold’s upward trend.

Performance (price return)

Source: Bloomberg, as of September 20, 2024

Macro developments

Canada – Inflation Slows to Target Level, Retail Sales Continue to Rise

Canada's inflation rate slowed to 2% in August, the lowest since February 2021, aligning with the central bank's target. Gasoline prices dropped by 5.1%, and clothing prices also declined. Shelter costs rose 5.3%, but overall core prices cooled to a 40-month low.

Retail sales in Canada grew by 0.5% in August, extending July’s 0.9% surge, driven by higher demand in motor vehicles, food, and personal care. This growth challenges calls for aggressive interest rate cuts.

U.S. – Retail Sales Remain Resilient, Fed Cuts Rates by 50bps

Retail sales edged up by 0.1% in August, beating forecasts of a decline. Miscellaneous stores, non-store retailers, and health stores saw gains, while gasoline stations and electronics sales dropped. Core sales, which are crucial for GDP, rose 0.3%.

The Federal Reserve cut interest rates by 50 basis points in September, the first cut since March 2020. The central bank plans additional rate cuts by year-end, with inflation and GDP growth forecasts revised lower.

International – U.K. Inflation Holds Steady in August, U.K. Retail Sales Surge Amid Warm Weather, Bank of England Maintains Interest Rates, Japanese Inflation Hits Highest Level Since 2023

The U.K.'s inflation rate remained at 2.2% in August, matching July's rate. Airfares and recreation costs rose, while motor fuel prices and restaurant costs fell. The CPI increased by 0.3% from the previous month.

U.K. retail sales jumped 1% month-over-month in August, driven by strong food and clothing sales. This marked the highest year-on-year retail growth since February 2022, boosted by end-of-season sales and favourable weather.

The Bank of England kept its rate unchanged at 5% in September after a cut in August. Inflation was 2.2% in August but is expected to rise by year-end. The bank also plans to reduce its government bond holdings by £100 billion over 12 months.

Japan's inflation rose to 3% in August, driven by sharp increases in electricity and gas prices. Food and household goods also saw higher prices. Core inflation reached a six-month peak of 2.8%, in line with market expectations.

Quick look ahead

As of September 20, 2024