Bonds or GICs: What’s the right investment for you?

Following the pandemic, rapid interest rate hikes and declining bond values drove many investors to seek better opportunities for cash and short-term fixed income. Guaranteed Investment Certificates (GICs) became more popular due to their appealing yields and ability to preserve capital—particularly attracting investors after substantial bond losses in 2022.

However, as inflation moderates and interest rates decline, the investing environment has changed. Investors may be wondering what the best fixed income strategy is for them. In this article, we outline a few of the ways that bonds and GICs differ and highlight how they might fit into an investor’s portfolio:

- Bonds versus GICs

- Historical performance of bonds vs. GICs

- How different scenarios can impact bonds

- Laddering: A classic risk-reduction strategy

- Why include fixed income in an investment portfolio?

- How to choose a fixed income investment

Bonds versus GICs

Bonds |

GICs |

|

|---|---|---|

Safety of capital |

No. Bond values fluctuate with market conditions. Bonds also have issuer default risk. |

Yes. A GIC has a guaranteed principal and return when held to maturity. They are also protected by Canada Deposit Insurance Corporation. |

Enhanced liquidity |

Yes. Bonds have greater flexibility and liquidity. Most bonds can typically be sold within a couple of days. |

No. GICs impose penalties for early withdrawals. |

Tax advantages |

Yes. Coupon/interest payments are taxed at the investor’s full marginal tax rate. However, capital gains from bond value appreciation are taxed at only 50% of the marginal tax rate. |

No. Outside of a registered account, GICs don’t offer any tax savings. Interest payments taxed at the investor’s full marginal tax rate. |

Reinvestment risk |

Yes (but less risk than GICs). Bond investors face less risk due to varying maturities and regular coupon payments. This income stream allows gradual reinvestment, reducing the impact of reinvestment risk in a declining interest rate scenario. As interest rates drop, bond prices generally rise, offering potential capital gains if sold. |

Yes. At maturity, GIC investors receive their principal along with accumulated interest, but in a falling interest rate environment, they might struggle to reinvest these funds at attractive rates. |

Higher potential return |

Yes. Opportunity for both income payments and capital gains. Bond liquidity also allows investors to respond more quickly to changing market conditions. |

No. Interest payments only, with investors locked in at the rate when the GIC was purchased. However, GIC returns are more predictable. |

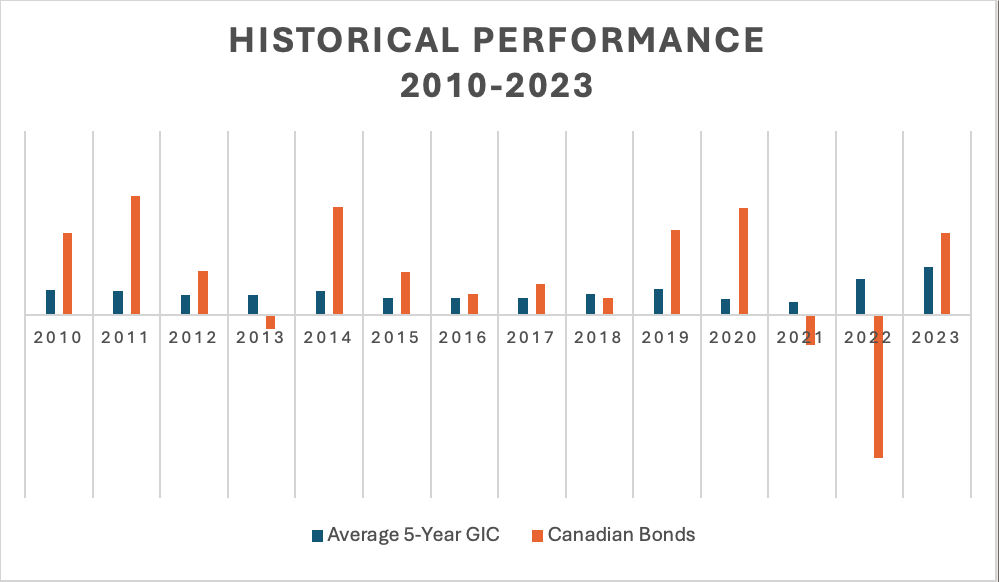

Historical performance of Bonds vs. GICs

If we look at historical performance, bonds have performed better over the long term, while GIC returns have been more consistent. The chart below compares the annual performance of Canadian bonds and the average 5-year GIC return. While bond returns are more volatile, GICs have only beat bond performance four times since 2010.

Data Source: NEI, “It Pays to Stay Invested”, p 11.

How different scenarios can impact bonds

In a high or rising interest rate environment, GIC yields tend to become more attractive to investors. However, bonds have historically offered higher return potential than GICs, There is an inverse relationship between bond yields and prices; during the interest rate hike cycle, many bonds trade at a discount, allowing investors to benefit from interest payments and capital gains as prices adjust back toward par. Here are a few possible scenarios that could have implications for bond prices:

If Canada enters economic recession and interest rates are cut further than anticipated:

- This would be positive for bond prices

If Canada cuts interest rates as expected:

- This would be positive for bonds, as they would continue to earn high yields

If inflation worsens, and interest rates stay where they are:

- This would be negative for bonds prices

Laddering: a classic risk-reduction strategy

Laddering works with both bonds and GICs to help reduce reinvestment and liquidity risk. Laddering involves staggering the maturity dates of your fixed-income investments to create a schedule for reinvesting the funds as each bond/GIC matures. By avoiding concentration of investments in a single time period or term, you help minimize the risk of having a large cash position coming due when reinvestment opportunities might be less favourable (such as during periods of low interest rates).

As each bond/GIC matures, the proceeds are invested in a longer-dated bond or GIC. This strategy benefits from the typically higher interest rates of longer-term bonds while ensuring that bond/GIC maturities are staggered. Bond or GIC laddering can be appropriate for long-term investors and those seeking a steady income stream.

A bond or GIC ladder is also beneficial from a liquidity standpoint. If you have multiple bonds/GICs at different terms, you have something maturing at regular intervals rather than having to cash in an asset early at an inopportune time, and where you might incur penalties

Laddering example: Let’s look at a GIC laddering example for an investor with $50,000 to invest in GICs.

Without GIC laddering:

- An investor would purchase a $50,000 GIC at the highest interest rate available (usually the 5-year rate).

- If they needed to access the money early, they would likely lose part of their interest and could incur other penalties.

- If they cashed out early and then wanted to reinvest their money back into a GIC, if interest rates have declined, they would have to reinvest at that lower rate and would lost out on the potential income.

With GIC laddering:

- An investor would start by purchasing five $10,000 GICs, each with maturities of one to five years.

- The next year, as the first GIC matures, the investor can then reinvest the $10,000 at the highest rate available (usually the 5-year rate). And this continues each year as the next GIC matures.

- If the investor needs to cash a GIC early, they will only incur penalties or lost income on that one GIC, not their entire investment.

- A ladder also provides greater flexibility. If the investor wanted to shift some of their money away from GICs, they would have that opportunity each time one matures.

Why include fixed income in an investment portfolio?

Fixed income for diversification purposes

Adding diversification to an investment portfolio is a common risk-reduction strategy. It means owning a variety of investments with differing characteristics – asset class, industry, geography – to help lower overall risk exposure to any one asset or group of assets.

All investments carry some risk – but they don’t all carry the same risks. Different asset types, different sectors, and different regions tend to perform differently in various market cycles. Diversification can be an effective way to reduce your overall investment risk and potentially smooth out your returns.

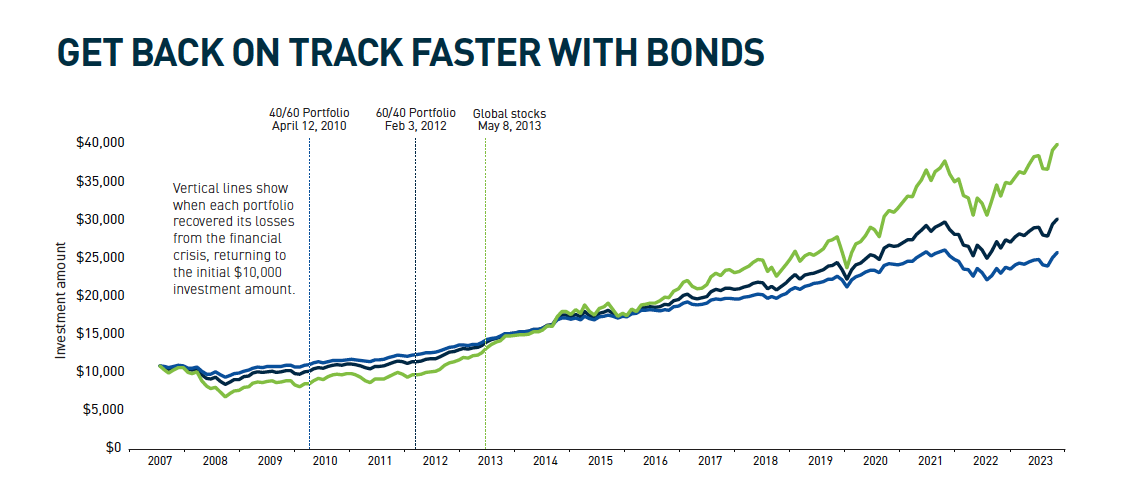

When your portfolio includes a variety of assets, some may perform well, and some may perform poorly – but it’s less likely that they will all perform poorly at the same time. What you earn on the investments that perform well can help to offset losses on the investments that perform poorly. Bonds and other fixed incomes can help diversify your stock portfolio and, historically, have helped investors recover more quickly from a downturn in the stock market (see below).

Source: NEI, “It Pays to Stay Invested”, p 9.

What this chart shows

During the Financial Crisis, global stocks (green line) fell further than a diversified portfolio made up of stocks and bonds. And even though stocks eventually caught up to the balanced portfolios, and surpassed them in recent years, they took significantly longer to recover from their decline. See how the portfolio with a 60% allocation to bonds (blue line) recovered its losses roughly two years earlier than the one with a 40% allocation to bonds (black line)? That’s how powerful bonds can be in offsetting the volatility of stocks.

If you’re concerned about how long it might take to recover from severe stock market losses, balance your portfolio with bonds. You may not earn as high of a return at the end of the day, but the journey there is likely to be more comfortable.

Fixed income as part of an income-generating strategy

Bonds and other fixed income assets also work well as part of an income-based investing strategy. If income was your goal, you would include assets – likely including bonds – in your portfolio that can deliver a consistent flow of passive income. While growth investors aim to achieve capital gains, income investors prioritize income and safety of principal. The regular cash payments provide an income that can be spent as it is needed and is often used as retirement income.

How to choose a fixed income investment

For shorter-term or for risk-averse investors, money market, GICs and other guaranteed investments offer safety and predictable returns. But for longer-term investors, bonds may be preferred due to the higher return potential, greater liquidity, and tax advantages.

There is no shortage of fixed income options available from Qtrade:

- Money Market assets include bank accounts, certificates of deposit, and money market mutual funds. Ideal for shorter-term investing because of their high liquidity.

- GICs come in a variety of terms and characteristics. Some may be cashable or convertible to other assets. Some may be linked to a stock index to enhance potential returns.

- Bonds come in all shapes and sizes, with different issuers (from governments and municipalities to corporations), different risk ratings (investment-grade to high-yield), and different features (convertible, inflation-adjusted, zero-coupon, etc.).

- Bond mutual funds or bond exchange-traded funds (ETFs) can offer diversification or specialization within the bond asset class to suit an investor’s goals and risk tolerance

Ultimately, the best choice of any investment – including fixed income investments – depends on your goals, your investing time horizon and your risk tolerance.

The information contained in this article was obtained from sources believed to be reliable; however, we cannot guarantee that it is accurate or complete. This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters.

Unless otherwise stated, mutual funds, other securities and cash balances are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer that insures deposits in credit unions.

Aviso Financial Inc. and Northwest & Ethical Investments L.P. are all wholly owned subsidiaries of Aviso Wealth Inc.